Last updated: June 2026

Most couples can talk about where to live, when to have kids, and what to name the dog. Money? That conversation gets postponed — until a credit card statement or a missed savings goal turns it into a confrontation instead of a discussion. If you’re figuring out how to manage money as a couple for the first time, the discomfort you feel is not a personality flaw. It’s a structural problem. Two people, two money histories, two completely different beliefs about what financial security even means, suddenly sharing one rent payment and one grocery budget.

This article gives you a working system. Not a lecture about the importance of communication. Not a generic budget template that collapses the moment one of you gets a bonus. A step-by-step framework you can actually implement — one that protects individual autonomy, prevents the most predictable sources of conflict, and grows with your relationship as it matures. You’ll leave knowing exactly which conversation to have first, which account structure fits your current stage, and what to do when a money disagreement escalates before either of you can stop it.

Have the Real Money Talk First

Before you open a spreadsheet, open a conversation — the right kind. Most couples skip straight to building a budget, which is exactly why money fights become a leading conflict driver in long-term relationships. A shared budget is only as strong as the assumptions underneath it. And those assumptions — about how much savings feels “safe,” about whether debt is shameful or just strategic, about who in your family growing up handled money and how — rarely get named out loud.

Try a 3-question Financial Belief Audit with your partner before you touch a single number. Sit down, no phones, and each answer these: What does financial security look like to you? What’s one money habit from the way you grew up that you want to keep? What’s one you’d like to leave behind? There are no wrong answers here. The goal isn’t to build consensus immediately — it’s to understand each other’s starting point. A couple where one partner grew up in a household that treated savings as everything and the other grew up where money was spent freely the moment it arrived will build a radically different budget if they never surface that gap first. This audit is the starting point competing advice almost always skips.

Choose the Right Account Structure for Your Stage

The standard debate — joint accounts or separate accounts? — is a false choice. It treats account structure as a one-time permanent decision, when it should actually evolve as your relationship does. Reviewing how couples structure accounts reveals that the source of most financial tension isn’t which model a couple picks, but the fact that they never revisit the model as circumstances change.

Think of it as three stages. The Independent Stage — typically when you’ve just moved in together — works well with fully separate accounts and a shared list of split expenses. Clean, low-commitment, minimal friction. The Hybrid Stage — often triggered by a significant shared financial goal, a formal commitment, or a major income shift — adds a joint account for shared bills while each partner keeps a personal account. This “yours + mine + ours” structure is the most conflict-resistant for couples with unequal incomes and different spending styles. The Unified Stage — usually after years together, a home purchase, or a child — merges more fully into joint finances with personal discretionary lines protected within the budget. The transition triggers matter just as much as the models themselves: moving in together is an Independent-to-Hybrid trigger; getting married or buying a home is a Hybrid-to-Unified signal. The account model you run on today should be a conscious choice for this chapter, not the default you landed on when you first combined a Netflix subscription.

Joint vs. Separate vs. Hybrid Accounts: Which Fits Your Stage

Choosing an account structure is one of the first practical decisions couples face — and one of the most misunderstood. There’s no universally right answer. The right structure depends on where you are in your relationship, how different your incomes and spending styles are, and how much financial overlap you actually want right now. The table below breaks down how each model works, who it serves best, and the trade-off you’re accepting when you choose it.

| Structure | How It Works | Best For | Main Trade-Off |

|---|---|---|---|

| Separate accounts | Each partner keeps their own accounts. Shared bills are split — either 50/50 or proportionally — via transfers or a shared payment method. | Couples who’ve just moved in together, those with very different spending styles, or anyone who values strong individual financial autonomy. | Requires ongoing coordination for every shared expense. No passive visibility into each other’s financial health. |

| Joint accounts | All income flows into shared accounts. All expenses — personal and household — are paid from the same pool. | Long-established couples with similar incomes, aligned spending habits, and a high degree of mutual financial trust. | Individual spending feels exposed and requires implicit (or explicit) approval. Can create power imbalances when incomes are unequal. |

| Hybrid (yours + mine + ours) | Each partner keeps a personal account. A third, joint account receives agreed contributions for shared bills, rent, savings goals, and joint purchases. Personal spending stays private. | Most couples — especially those with unequal incomes, different discretionary habits, or a relationship that’s still establishing its shared financial identity. | Requires upfront coordination to set contribution amounts and decide what counts as “shared.” Needs revisiting when incomes shift. |

One detail most couples overlook: the model you start with doesn’t need to be permanent. A hybrid setup in year two of living together may evolve naturally into a more unified structure after a home purchase or a child. The trigger for changing models is a shift in shared financial stakes — not a calendar date or an arbitrary relationship milestone. Build a review into your annual money conversation, and you’ll catch the moment a structure stops fitting before it starts generating friction.

Build a Shared Budget Without Losing Financial Autonomy

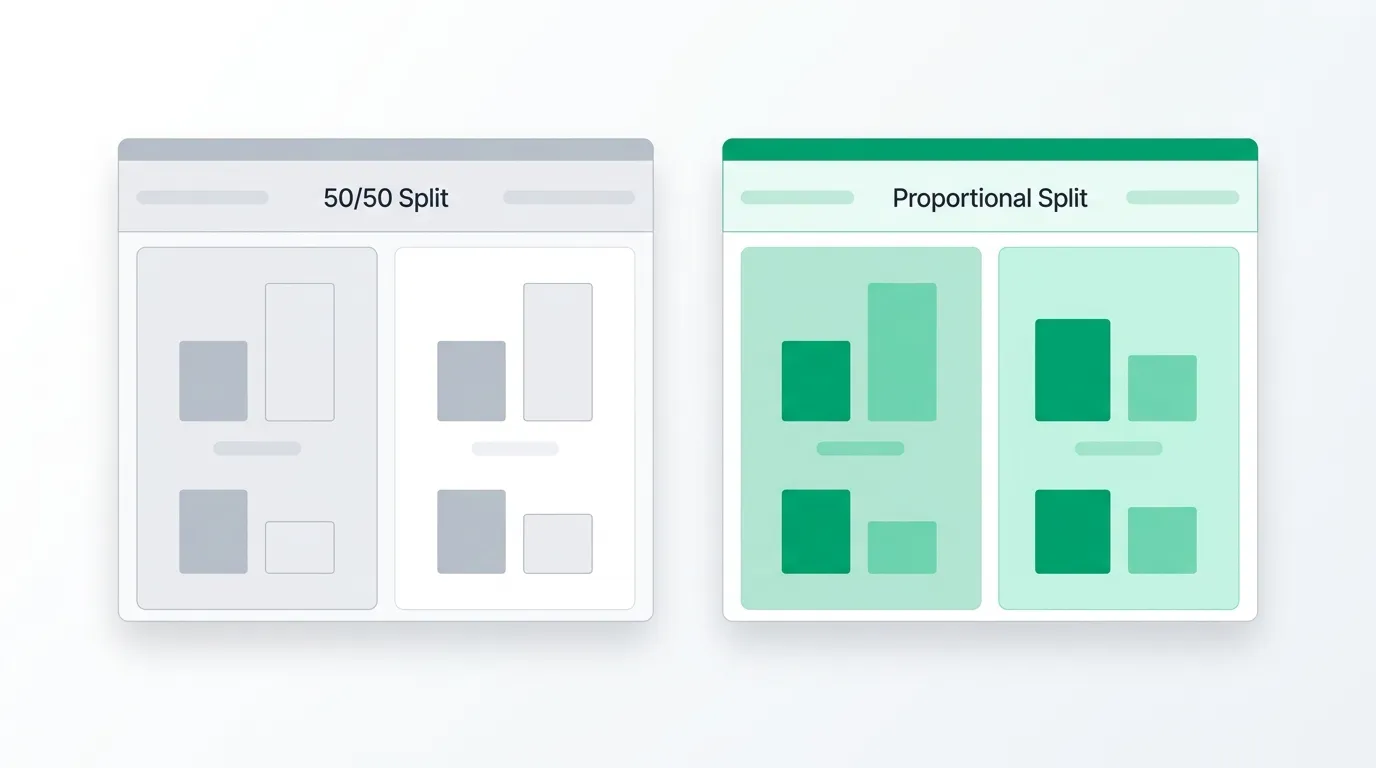

Here’s where most financial advice gets technically correct but emotionally tone-deaf. A 50/50 expense split sounds fair. It isn’t — not when incomes differ. If you earn $6,000 a month and your partner earns $3,000, splitting a $3,000 rent bill equally means you’re contributing 25% of your income while your partner contributes 50% of theirs. That’s not fairness. That’s a slow-building resentment generator. The proportional model fixes this: each partner contributes their income share of combined household expenses. If you earn 67% of the household income, you cover 67% of shared costs. The math is simple; the fairness is felt immediately by both sides. For a deeper dive into structuring your full personal budget, a solid personal budgeting framework can complement the couple-specific system you’re building here.

The second structural move that prevents more arguments than almost anything else is the personal allowance. Set a fixed amount — agreed between both of you — that each partner spends however they want, no reporting required. Yours might go on coffee and concert tickets. Your partner’s on sports gear and video games. Neither of you owes the other an explanation. This single line item in your shared budget functions as a psychological safety valve: it removes the feeling of financial surveillance that causes one partner to hide purchases and the other to play financial cop. Budget structures that include individual discretionary allowances consistently show lower conflict rates than those that demand joint approval for every personal expense. Small. Non-negotiable. Effective.

Build a Conflict-Proof System for Financial Disagreements

Even a well-designed financial system breaks down under emotional pressure. Two people with different risk tolerances, different spending habits, and shared financial stakes will disagree. That’s not a sign your relationship has a money problem — it’s a sign you’re paying attention. The question isn’t how to avoid financial disagreements. It’s what you do when one starts escalating.

Most couples have zero pre-agreed protocol for this moment. So they improvise, and improvisation under stress defaults to blame. The solution is a Financial Time-Out Protocol — a 4-step framework you agree on before any conflict arises. Step one: either partner can call a pause by using a single agreed signal phrase (“let’s table this”). No debate about whether to pause — that’s the rule. Step two: a 24-hour waiting period, no discussion of the topic. Step three: reconvene with data, not feelings as the opener — bring the actual numbers, not a recap of the argument. Step four: if you’re still deadlocked, a pre-agreed decision rule kicks in (a coin flip for low-stakes decisions; a third-party financial advisor for large ones). Pair this with a fixed monthly money date — 35 minutes, same day each month, agenda-driven — and you shift your financial relationship from reactive to proactive. The agenda doesn’t need to be complicated: 10 minutes reviewing last month’s shared spending, 5 minutes checking savings progress, 5 minutes each partner reports their personal allowance status, 10 minutes previewing upcoming large expenses, 5 minutes setting one micro-goal for the next 30 days. Couples who treat financial conflict as a system problem to solve — not a character flaw to assign — argue less and save more.

Frequently Asked Questions

Should couples have joint or separate bank accounts?

Neither structure is objectively superior — the right choice depends on your relationship stage, income gap, and how aligned your spending styles are. Separate accounts work well early on or when autonomy matters most. A joint account fits couples who’ve built deep financial trust and have similar earning power. For the majority of couples — especially those navigating an income difference or mismatched habits — the hybrid model (personal accounts plus one shared account for bills) offers structure without surveillance. The most important thing isn’t which model you pick; it’s that you pick it consciously and revisit it when circumstances change.

How should we split bills if we earn different amounts?

Use a proportional contribution model rather than a flat 50/50 split. Calculate each partner’s share of combined household income, then contribute that same percentage toward shared expenses. If you earn 65% of total household income, you cover 65% of shared costs — your partner covers the remaining 35%. This removes the quiet resentment that builds when one partner pays the same dollar amount but at a much higher personal cost. The formula scales automatically whenever either income changes, which makes it worth revisiting quarterly rather than treating it as a one-time setup decision.

What percentage of income should go to shared expenses?

There’s no fixed number that works for every couple, but a useful starting range is 50–70% of combined take-home pay directed toward shared household costs — rent or mortgage, utilities, groceries, insurance, shared savings. The remainder stays in each partner’s personal column. Couples in high-cost cities or with significant shared debt tend to land at the higher end of that range early on. What matters more than hitting a specific percentage is that both partners feel the split is fair relative to what they’re each earning and spending personally. Revisit the allocation any time your combined income shifts by more than 10%.

How do we handle debts each partner brought into the relationship?

Pre-relationship debt belongs legally to the partner who incurred it — unless you co-sign, refinance, or formally combine it. But financially, it affects both of you: debt repayment reduces what’s available for shared goals, which means it’s a shared planning concern even if it’s not a shared legal liability. The honest approach is to disclose all existing debt during the Financial Belief Audit stage — amounts, interest rates, and current repayment plans. From there, decide together whether the debt-free partner temporarily reduces their shared contribution to offset repayment pressure, or whether both contribute toward faster payoff. The decision itself matters less than making it explicitly, because unspoken assumptions about debt are where real resentment grows.

How often should we have a money check-in?

A monthly money date is the minimum that keeps a shared financial system functional — short enough to catch problems early, spaced far enough apart that it doesn’t feel like constant monitoring. Keep it to about 35 minutes with a simple agenda: review last month’s shared spending, check progress on savings goals, flag any large upcoming expenses, and set one small financial priority for the next 30 days. Add a longer quarterly session (60–90 minutes) to adjust contribution amounts, assess whether your account structure still fits, and look at progress toward bigger goals. Couples who schedule these check-ins in advance — same day each month, treated like any recurring appointment — argue significantly less about money between sessions than those who address finances only when something goes wrong.

What if we have completely different spending styles?

Start by recognizing that neither style is objectively right. A tendency to save aggressively isn’t a virtue; a willingness to spend on experiences isn’t recklessness. They’re different risk tolerances shaped by different histories. The structural fix is a personal allowance — a fixed, individually controlled spending amount each partner manages without requiring the other’s approval. Whatever your natural style is, it operates freely within that boundary. For shared purchases above a threshold you both agree on upfront (a specific dollar amount that feels meaningful but not restrictive), you discuss before spending. That one rule does more practical work than any number of conversations about getting on the same page.

Conclusion

Managing money as a couple is less about finding the perfect budget template and more about building a shared language around something both of you learned to feel — not just think — about long before you met. The system outlined here gives you the structure: a belief audit before the spreadsheet, an account model that evolves with your relationship, a budget that protects individual autonomy, and a pre-agreed protocol for when things get heated. None of it requires financial expertise. All of it requires honesty. Start with one conversation — not about numbers, but about what money has always meant to you — and build from there.

References

External sources

- How to Budget as a Couple Without Fighting About Money | DollarFlourish — https://dollarflourish.com/budgeting/budget-as-a-couple